The Most Honest AI Analysis of the Year (and What Everyone Needs to Know)

Benedict Evans just published the most honest AI analysis of the year. Here's what everybody wants to know.

Benedict Evans: The Man Behind the Deck

Benedict Evans has called technology shifts right more consistently than almost anyone alive. If this is the first time you are hearing his name, you are about to read something full of gems.

He spent 25 years as one of the sharpest analysts in tech, across equity research, strategy consulting, and a long run as a partner at Andreessen Horowitz. Twice a year he publishes a macro deck on where technology is heading. His 2013 “Mobile Is Eating the World” became required reading for the smartphone wave while it was still forming, and he called mobile before most people knew what mobile meant.

His weekly newsletter reaches around 200,000 readers, and he has presented for Alphabet, Amazon, LVMH, and Goldman Sachs. When Evans publishes, serious people in tech read it carefully and argue about it for months. “AI Eats the World” is his most consequential deck yet, because it does not tell you AI is revolutionary. It forces you to ask which part of the revolution you are in, and whether the part you are betting on is the part that wins.

together with Hard Skill Exchange:

Evans makes you pick which part of the AI shift you are betting on. Here is one that is already arriving: your next customer may not be human.

Hard Skill Exchange is running a FREE virtual AI summit on exactly that. Agent-to-Agent GTM, where the people building machine-native go-to-market show what breaks when software becomes the buyer, the seller, and the decision maker.

▫️ 3 days, fully virtual, free for everyone, with no ticket and no travel

▫️ Agent-native GTM playbooks for a market where buyers skip ads, brands, and funnels

▫️ The operators defining the category before the consensus catches up

It runs live June 23 to 25, and then it is gone. Your next customer may not be human, so it would be a mistake to sit this one out:

Table of Contents

Platform Transitions Eat Their Parents

The Financial Model Is Quietly Breaking

900 Million Users. Almost Nobody’s Hooked.

Models Are a Commodity. Deal With It.

The Right Question About Jobs

The Uncomfortable Math

1. Platform Transitions Eat Their Parents

Every 10 to 15 years, the tech industry doesn’t just add a new layer. It rewrites the rules of the previous one, and the prior winners often don’t survive the rewrite.

Evans opens the deck here, and it deserves more than a quick nod.

The historical progression runs from Mainframes to PCs to the Web to Smartphones to Generative AI. Each transition didn’t just produce new companies. It made the dominant players of the prior era structurally irrelevant in ways they couldn’t have anticipated or defended against.

Microsoft went from owning essentially all of global computing in 2000 to less than 15% of computing units by 2025. Not because Windows got worse. Because the iPhone redefined what “a computer” was, and Microsoft had no answer for it.

This is what makes the current spending war legible. The CEOs committing hundreds of billions are not doing it because the returns are obvious. They are doing it because they have studied that chart and have no interest in becoming the next example on it.

Sundar Pichai said the risk of under-investing is significantly greater than the risk of over-investing. Zuckerberg said the worst case is that they “just prebuilt for a couple of years.” Those are not confident statements. They are the sound of people who know what happens to the unprepared.

The question nobody is asking loudly enough

What Evans doesn’t say explicitly, but the framing implies: the companies most at risk here are not the ones who refuse to invest. They are the ones who invest in the wrong layer.

Platform transitions have a habit of making yesterday’s moat look like a liability, and there are a lot of very expensive bets being placed right now on layers that may not be where the value ends up.

The companies that dominated the PC era built for PCs. The companies that dominated mobile built for mobile.

Winning the current infrastructure race does not guarantee winning what comes after it. That distinction is what the rest of the deck is really interrogating.

2. The Financial Model Is Actually Breaking

The four biggest tech companies, Meta, Microsoft, Alphabet, and Amazon, are planning a combined $700 billion in capital expenditure in 2026 alone.

The entire global telecom industry spends around $300 billion annually. Big Tech has entered that tier of physical investment almost overnight, and the balance sheets are starting to show it.

For most of their existence, these were asset-light businesses. Software scales without proportional physical investment. High margins, minimal infrastructure, free cash flow that funded buybacks, acquisitions, and everything else. That was the entire premise of their valuations, and it is now under serious pressure.

Meta and Microsoft are both approaching 55% of revenue going to capex in 2026. In 2015, Meta was spending around 10%. These numbers do not look like software companies anymore. They look like the capital structures of the industries they used to disrupt.

When a company’s cost structure changes this radically this fast, something has to give. Either the revenues scale to justify it, the margins compress, or the valuation assumptions get repriced. Right now, markets are betting hard on option one.

The deeper issue is that this investment is not discretionary anymore. You can’t half-build the infrastructure. You can’t decide in two years that you over-invested and sell the data centres back.

This is a one-way door, and the world’s most valuable companies walked through it while telling their shareholders it was the obvious move. Maybe it was. But the size of the bet means there is no graceful exit if the thesis is wrong.

A quick one, courtesy of Hard Skill Exchange:

While Big Tech bets $700B on the infrastructure, the go-to-market layer on top of it is already changing

The free Agent-to-Agent GTM Summit covers what happens when software becomes the buyer. 3 days, fully virtual, free for everyone, live June 23 to 25.

3. 900 Million Users. Almost Nobody’s Hooked.

ChatGPT has over 900 million weekly active users, but only 5% of them are paying. Evans shows the growth curve and it looks extraordinary, right up until the next slide reframes everything.

OpenAI’s own “Wrapped” data tells a different story. For at least 80% of users, total usage across all of 2025 was under 1,000 prompts. That is fewer than 3 per day. For the vast majority of people who “use” ChatGPT, it is something they open occasionally, the way you open a dictionary.

Evans calls this “a mile wide and an inch deep.”

At the end of the day, this is not product-market fit. Product-market fit is when people use something daily without being reminded it exists, when they complain loudly if it goes down, when they genuinely cannot describe their workflow without it.

The comparison to smartphones cuts in the wrong direction. Within three years of the iPhone, people were sleeping next to their phones. Within three years of ChatGPT, 80% of users are sending fewer prompts per day than they send text messages per hour.

The enterprise story mirrors the consumer one.

Bain’s data shows that across every major business function, the gap between “in pilot” and “in production” is enormous.

Everyone has a proof of concept. Almost nobody has something running at scale that has actually changed how the business operates.

Pilots are easy to start and hard to kill. They generate internal goodwill, satisfy board questions about AI strategy, and require minimal organisational change.

Getting from pilot to production means redesigning workflows, retraining people, and accepting that the model will sometimes be wrong. Most companies haven’t started that part.

The one real exception is coding. Enterprise AI spending on software development is roughly five times the next biggest category.

Among developers, AI has clearly become a daily essential. But coding is one profession, and the distance between “coding is transformed” and “work is transformed” is still vast.

4. Models Are a Commodity. Deal With It.

This is the part of the deck the industry is not engaging with honestly, and it has direct consequences for how you think about the biggest valuations in private market history.

Look at the benchmark chart for frontier LLMs. OpenAI, Anthropic, Google, Meta, the Chinese labs: scores are converging at the top. For most general use cases, the models are now functionally interchangeable.

And there are no network effects. A model doesn’t get better because more people use it. It doesn’t accumulate data about you that makes switching painful.

Evans draws the comparison to mobile telecom infrastructure, and it is the most pointed analogy in the deck.

Global mobile data traffic exploded over 15 years. Global telco stocks went essentially nowhere over the same period. The companies that built the pipes carried all the value but captured almost none of it.

Infrastructure businesses at scale, serving commodity demand, get priced like utilities. Necessary, steady, and low margin. Sam Altman’s “intelligence as a utility like electricity or water” is more accurate than he probably intends. Utilities are worth owning. They are not worth $850 billion.

Electricity producers don’t capture the value created by the industries running on their power. That value goes to whoever builds the product people actually use every day.

The interesting question is not who trains the best model. It is who builds the thing on top of it that becomes genuinely indispensable.

5. The Right Question About Jobs

Most of the public conversation about AI and employment is asking the wrong question. People want to know which jobs disappear. So the ultimate question according to Evans is:

Is this a job, or is it a task?

A task is a defined operation with a known input and output. A job contains judgment, relationships, and decisions made under genuine ambiguity. That’s a huge distinction when we talk about AI.

In 1950, there were nearly 100,000 elevator operators in the United States. Otis automated the elevator, and the profession was gone within a decade, because the job was just a task.

There was nothing else there. But accountants grew as a share of US employment for decades after software automated their core computational work, because what accountants actually do expanded as the cost of calculation fell.

Before grocery barcodes in 1974, the average US supermarket stocked around 8,000 products. By 2010, that number was 50,000. Automated inventory management didn’t just make stocking cheaper. It made a level of variety that was previously impossible suddenly achievable. The free task unlocked something that couldn’t exist before.

The live test nobody wants to talk about

Evans points to the Philippine outsourcing industry as the most immediate real-world test of this framework.

Two million people, 8% of GDP, built entirely on a skill and income arbitrage that AI is now directly threatening.

Whether those roles survive depends entirely on whether they are tasks or jobs. Some are pure tasks with defined inputs, defined outputs, no judgment required. Those are (or will be) gone.

Others involve enough human context, relationship management, and situational reading that they are genuinely jobs. Those will change, probably dramatically, but they won’t simply disappear.

Anyone telling you they know exactly which category any given role falls into is guessing. The honest answer is that nobody knows yet, and the outcome will vary enormously by industry, company, and how aggressively employers choose to act.

6. The Uncomfortable Math

One slide in Evans’ deck is more unsettling than any of the capex charts.

OpenAI and Anthropic are each valued in private markets at roughly $850 to $900 billion. The total market capitalisation of every US venture-backed IPO from 1995 to 2000, the entire dot-com boom adjusted to today’s dollars, was around $780 billion.

Two companies, each worth more than an entire era of internet investment, with business models nowhere near equilibrium, in a model layer that is commoditising in real time.

There are three ways to make that math work:

The valuations are irrational and a correction is coming.

The commodity thesis is wrong and one or both labs builds a lasting moat through something not yet invented.

The application layer ends up being worth so much that the model providers capture enough of it to justify the numbers.

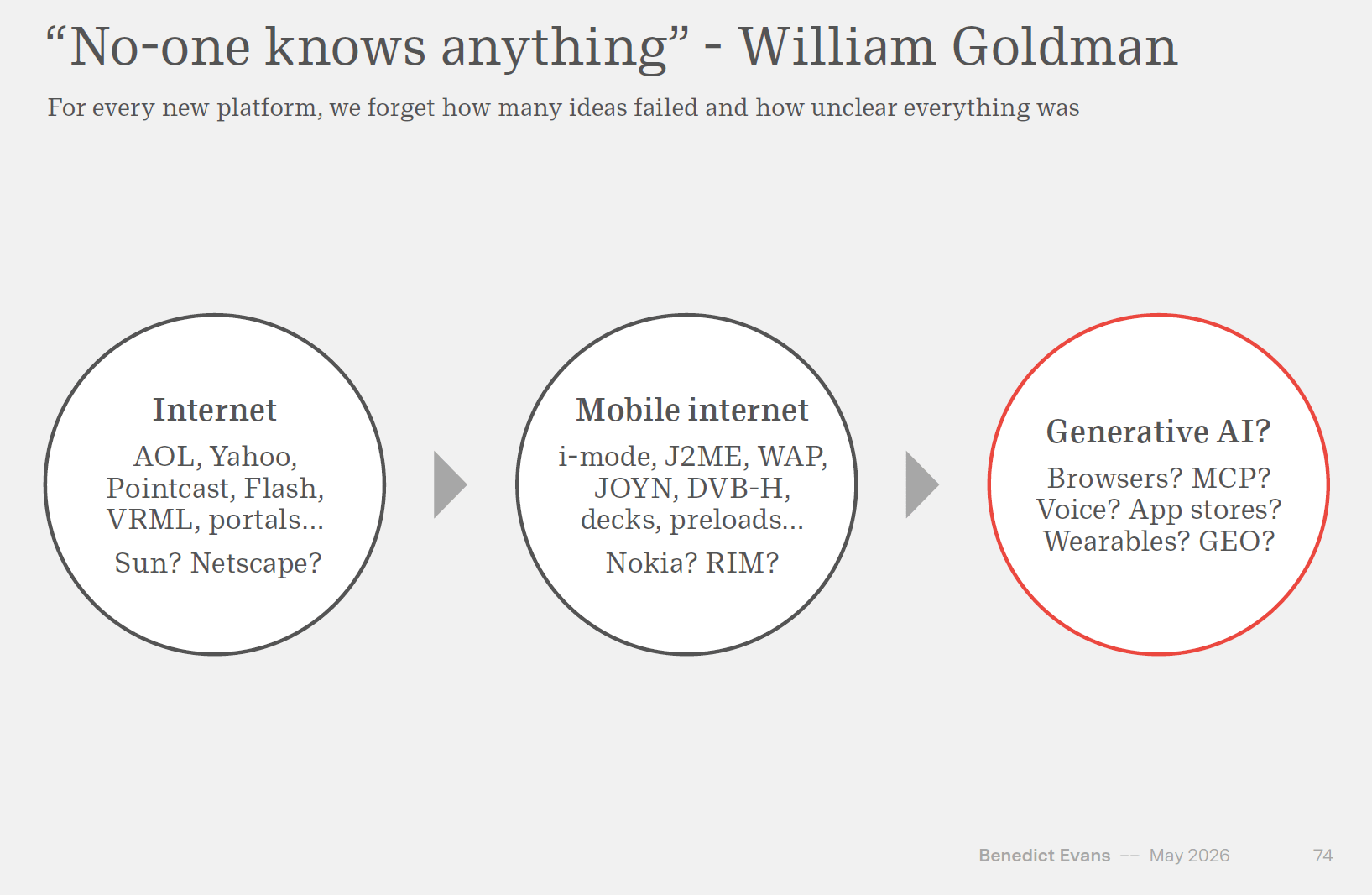

Evans ends with William Goldman’s line: “No one knows anything.” The internet era produced AOL, Yahoo, and Pointcast before it produced Google. The mobile era produced WAP and Nokia before it produced the iPhone.

Every platform transition has false starts, confident predictions that age terribly, and a long stretch of genuine uncertainty before the real picture emerges. This one will be no different.

The infrastructure is real. The growth is real. The most important chapter of this story hasn’t been written yet.

The accountant who saw VisiCalc in 1979 and understood what it meant built something lasting. The one who called it a curiosity missed everything that followed.

That decision is sitting in front of every operator and founder reading this right now.

AI's future won't be decided by who builds the smartest model, but by who solves the most valuable business problems. Insightful analysis.

Great article. Rooted in reality. This doesn't mean that LLMs are not valuable. They're fantastic and powerful tools that have changed productivity significantly for those that use it appropriately. But this accurately support the claim that AI has been and is over hyped.